On February 15th 2021, export quotas on wheat, rye, maize, and barley entered into force in Russia. Russia also imposed customs tariffs and prohibitive duties amounting to 50% of customs value on these products.

WHAT DOES THIS MEAN FOR GEORGIA?

In general, the introduction of customs tariffs or quotas on exports is a part of a protectionist policy and is, more often than not, directed towards the protection of local producers and markets. Export quotas entail restrictions on the number of specific goods and services within an outlined period of time with the aim of maintaining low prices on respective goods for local consumers. Unlike quotas, customs tariffs are imposed as a means of generating state revenue, which may subsequently be spent on strengthening local producers. Traditionally, imposing export restrictions translates into growth of local supply and price reduction in exporter states, which is mirrored by an increase in prices of imports and a decrease in demand from importer states. In theory, there are two central factors for this effect:

- International Prices – Export restrictions introduced by large exporter states impact international prices. Since Russia is one of the biggest exporters of wheat, the imposition of restrictions on its exports limits wheat supply on international markets, therefore increasing prices. Importer states may diversify their import markets, but due to the increase in international prices, they still have to spend more.

- Expectations – Imposition of export quotas creates expectations of supply deficits, further increasing prices.

It is also worth noting that an increase in import prices may support the growth of local production in importer states.

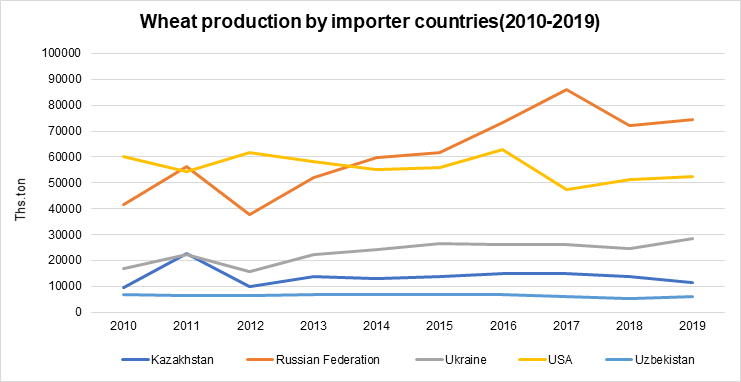

According to data from the UN Food and Agriculture Organisation (FAO), in 2019 China was the biggest producer of wheat with a 17% share of global production followed by India (14%), Russia (10%), the US (7%), and France (5%). Georgia imports most of its wheat from Russia. In 2020, 95% of total wheat imports came from Russia, with 4% imported from the US. In the period of 2012-2015 Georgia imported large quantities of wheat from Kazakhstan and Ukraine, however, Russian wheat quickly replaced these markets (Geostat, 2021), which is not surprising, as Russia outperforms Georgia's other trading partners in terms of wheat production (Table 1).

Figure 1. Wheat production in importer countries (2010-2019)

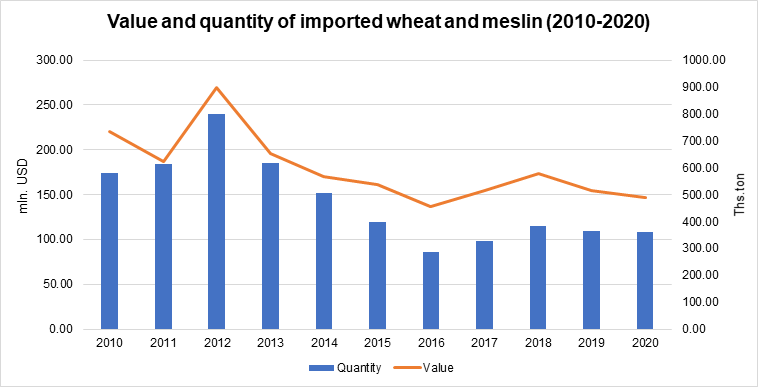

It is significant that, in general, both quantity and prices of imported wheat were characterised by a downward trend in the period of 2010-2020 (Table 2), which can be explained by increased local production and, thus, a rise in self-sufficiency coefficient (2010 – 6% and 2019 – 15%) (Geostat, 2021).

Figure 2. Quantity and value of imported wheat and meslin, 2010-2020

Wheat import prices (HS1001), which fluctuated from $190-280 per tonne in the period of 2012-2020, show a downward trend. During the last two years the price reached its minimum and amounted to $213 and $219 per tonne in 2019 and 2020 respectively. Import prices of hard wheat are relatively higher (except for wheat seeds, HS100119), reaching $226 and $252 per tonne in 2019 and 2020 respectively (Trade Map, 2021).

A review of wheat trading statistics revealed that Georgia is dependent on the Russian market, with a low level of market diversification. Therefore, the imposition of trade restrictions by Russia may result in a rise in the prices of bread and pastry in Georgia. In order to avoid such outcomes, the Government of Georgia took the following measures:

- Developed a price subsidy programme for wheat flour: In order to maintain the retail price of bread, on November 30th 2020 the Government of Georgia issued an ordinance regarding the adoption of a state subsidy programme for wheat flour. The subsidy amount constituted of no more than 10 GEL per one 50-kilogramme sack of first-grade wheat flour. Within the framework of the programme, first-grade wheat flour sold between December 1st 2020 and March 31st 2021 is subsidised. The budget for the four-month-long subsidy programme amounted to 10 mln GEL.

- Subsidised utility expenses for food manufacturers, including bakeries: According to a decision made during a session of the Georgian National Energy and Water Supply Regulatory Commission (GNERC) held on December 29th 2020, starting from 2021 electricity consumption tariffs increased in both Tbilisi and Georgia’s regions. Due to the pandemic, the Government of Georgia decided to subsidise 50% of the increased electricity tariffs throughout 2021 for all food production companies, including bread producers.

- Employed an import market diversification strategy: In order to decrease dependency on the Russian market, 23,400 tonnes of wheat were imported from the US, which amounts to a small fraction of the overall average annual import quantity (approximately 500,000 tonnes). It is important for Georgia to consider other trading partners (e.g. Kazakhstan and Ukraine).

WHAT OUTCOMES DID THE STATE PROGRAMMES HAVE?

According to the Association of Wheat and Flour Producers, due to the import restrictions, the Association has increased its storage of wheat, for the time being maintaining bread prices with the support of the subsidy programme. However, due to the aforementioned restrictions, an increase in wheat prices is expected. The increase in input prices will, thus, be reflected in an increase in bread prices. It should be noted that bread producers in Georgia plan to increase bread prices starting from April. They state that the price of bread is likely to increase due to higher prices on petrol and yeast, as well as increased electricity tariffs.

In order to maintain bread prices, it is recommended to:

- Develop local production: While a large number of small-scale agricultural holdings makes wheat production difficult, outdated methods of production also harm this sector. The productivity of wheat in Georgia amounts to 2.3 tonnes per ha, while Georgia’s partner states have higher indicators: the US – 3.4 tonnes per ha, Russia – 2.7 tonnes per ha, Ukraine – 4.1 tonnes per ha (FAO, 2021). Although Georgia’s indicator is similar to Russia’s, Russia has the advantage of large-scale production. Due to the lack of large arable land areas, it is important for Georgia to focus on increasing productivity.

- Seeking alternative markets for import diversification: One alternative may be focusing on the Kazakh and Ukrainian markets and negotiating possible ways to decrease the cost of transporting wheat to Georgia with state and private sector representatives from these countries. In October 2019, a mechanism for subsidising the transportation cost of Kazakh wheat was supposed to be activated by the Kazakh government if Kazakh companies expressed an interest in exporting wheat to Georgia. As evidenced by trade statistics, imports of Kazakh wheat have not changed much since 2019, which can be explained by three factors (or a combination of them): (1) low quantity of wheat-production in 2019; (2) the COVID-19 pandemic and associated restrictions; (3) need to modify/improve the stimulating mechanism.

The Ukrainian market is of no less significance. Ukraine produces more wheat than Kazakhstan. Additionally, during the recent decades, both production and exports of Ukrainian wheat are characterised by an upward trend. For both Russia and Ukraine, the main export markets include Egypt, Bangladesh, and Turkey, with the Georgian market taking a minor position among Ukraine’s wheat export markets. It is important to better research the Ukrainian market and cooperate with both state and private sector representatives in Ukraine.

The views and analysis in this article belong solely to the author(s) and do not necessarily reflect the views

of the international School of Economics at TSU (ISET) or ISET Policty Institute.

15

November

2021

15

November

2021

{kind=link}