If you visit any post-Soviet country after spending some time in the West, one thing strikes you immediately: the average age of visible poverty. Not only are you more likely to see old people begging on the streets, but old people are also dressed more poorly, and tend to buy the cheapest things on the market.

Georgia is no exception. The main source of income for most Georgian elderly is the state pension. The level of benefits is extremely low and can barely lift people up above the poverty line. And yet, for many households, the state pension is the only barrier that separates them from extreme poverty. In 2014, pensions were the main source of income for as many as 30% of Georgian families1, significantly reducing the incidence of poverty among the population.

Meager as the pensions are, an immediate concern for policymakers is whether these benefits can be sustained at least at their current levels in the near future. Another concern is how to make sure that future generations of Georgian retirees are not only able to survive but actually have a decent life.

CAN THE GEORGIAN PENSION SYSTEM BE SUSTAINED IN THE NEAR FUTURE?

Currently, Georgia has the so-called pay-as-you-go (PAYG) system, according to which pensions are paid from tax revenues collected from the current taxpayers. In order to keep this system running and the pension benefits constant, the “tax base” – that is the number of employed people multiplied by the salaries they receive – should grow at least as fast as the number of pensioners.

So far, this has not been a problem. The number of pensioners grew by approximately 1% a year, and the tax base was sufficient to finance even real (beyond inflation rate) increases in pensions. Going forward, the system will be sustainable if the real growth rate of the economy exceeds the rate of growth in the number of pensioners.

FROM SUBSISTENCE TO DECENT OLD-AGE LIFE

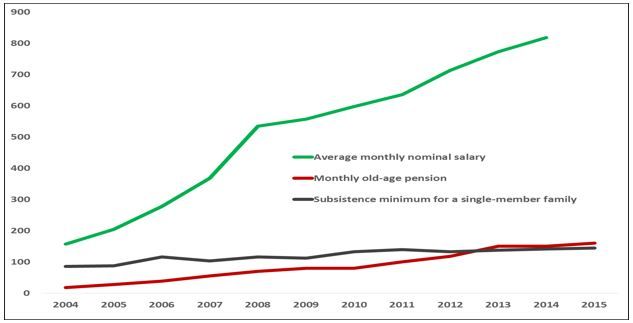

In 2013, Georgia’s average monthly pension finally broke the subsistence minimum threshold for a single-member household. However, in real terms, pensions still amount to a marginal share (10-20%) of the average monthly salary. This is of course very far from “decent” old-age provision, normally considered to be equal to about 50% of the average monthly income in a country.

It would be naive to think that a large increase in monthly pension payments, well above the subsistence minimum level, is feasible in the near future. The main problem is that the “average salary” that we see on the graph is earned by hired workers – a mere 16% of the population. The vast majority of Georgia’s working-age population consists of self-employed workers in low-paying jobs and the unemployed.

As the population ages, even the current system will be strained. For one, in 2014 there were 2 pensioners per 5 employed2 and approximately 1 pensioner per 1 hired worker in Georgia. As life expectancy improves, pension benefits will need to be paid out for longer and longer periods of time. Consequently, the burden of pensions will become increasingly heavier for the state budget.

This problem is not unique to Georgia. Other countries in the world – Japan, the US, UK – all face similar problems. In the United State, the government-provided benefits for people over 62 are considered to be a supplement, but not the only source of “decent” old-age income. There is an expectation that people will also save out of their current income to have a decent living in retirement. That is why many countries at different points in time started implementing pension savings schemes. A similar solution was recommended to Georgia by the World Bank in 2014: “Georgia public expenditure review: Strategic issues and reform agenda”.

PROPOSED REFORM: RISKS AND OPPORTUNITIES

The proposed reform envisages the introduction of the 2%+2%+2% contributions system. This would work as follows. Employees would be automatically enrolled in the pension scheme unless they refuse to join. Those enrolled would contribute 2% of their salary to the fund, with the government and employers each adding another 2%.

One important aspect of the reform is that the pension payments under the proposed system will not be a substitute, but rather a complement to the state pensions, as they exist today.

THE OPPORTUNITIES

1. The proposed change is essentially a means of encouraging people to put money aside for retirement. It is seen as a discipline tool for that pensioners-to-be who can save, but find it hard to resist the temptation to spend.

2. The sum that people will save through the new scheme will be exempt from taxes. The employees’ contributions will be matched by employers and the government, thus boosting savings in the economy.

3. The funds collected through the pension savings scheme can be used for investments in long-term projects inside the country. This could promote growth, especially in our investment-hungry economy, where the low level of savings is a real problem.

THE RISKS

1. The new scheme will only work for hired workers. In 2014, hired workers constituted about 16% of the population and only 40% of all employed persons. It would be a challenge to engage the “self-employed”, who will be among the poorest and the most vulnerable in the future pensioners’ pool.

2. The proposed scheme envisages a 2% contribution by employers – essentially a tax that may discourage businesses from hiring additional labor.

3. If the proposed pension fund invests only in Georgia, the returns can be high but also highly risky. In order to diversify the risk, the pension fund would have to take at least a part of the savings out of the country.

4. Last but not least, whether the proposed scheme is successful or not would depend on people’s trust in the pension fund’s management and the Georgian financial system. Establishing such trust may be a challenge: in 2013, only 35% of the population reportedly trusted the banking system, and only 39% trusted the executive government (data from the Caucasus Barometer).

OTHER OPTIONS TO CONSIDER

A standard way to evaluate the impact of such a far-reaching reform is to perform a Regulatory Impact Assessment (RIA) which requires an analysis of alternatives. If the goal of the reform is to lighten the fiscal burden of pension spending, then one needs to also discuss and evaluate the potential impact of raising taxes and/or increasing the pension age (however unpopular such measures maybe).

It would be very important to test any future pension schemes by launching pilot projects involving, for example, government employees. Different schemes may achieve different participation rates. Thus, one could consider allowing the use of pension savings to cover medical costs and/or investment in housing as a means of increasing the number of participants (as was the practice in Singapore).

Finally, keeping the status quo is always an option. It may be the case that the proposed scheme is not worth the cost and that the current system is good enough for Georgia, where family ties are strong and the elderly are rarely left completely alone.

In any case, being wrought with risks and policy trade-offs, any future pension reform must start with a healthy and well-informed public debate. The question is of crucial importance: how can we ensure decent retirement for Georgia’s elderly without putting an undue burden on our children and grandchildren?

1 An author’s estimate based on GeoStat’s Integrated Household Survey

2 This includes both the self-employed and hired workers.

The views and analysis in this article belong solely to the author(s) and do not necessarily reflect the views

of the international School of Economics at TSU (ISET) or ISET Policty Institute.

02

July

2024

02

July

2024